Market Overview and Growth Outlook

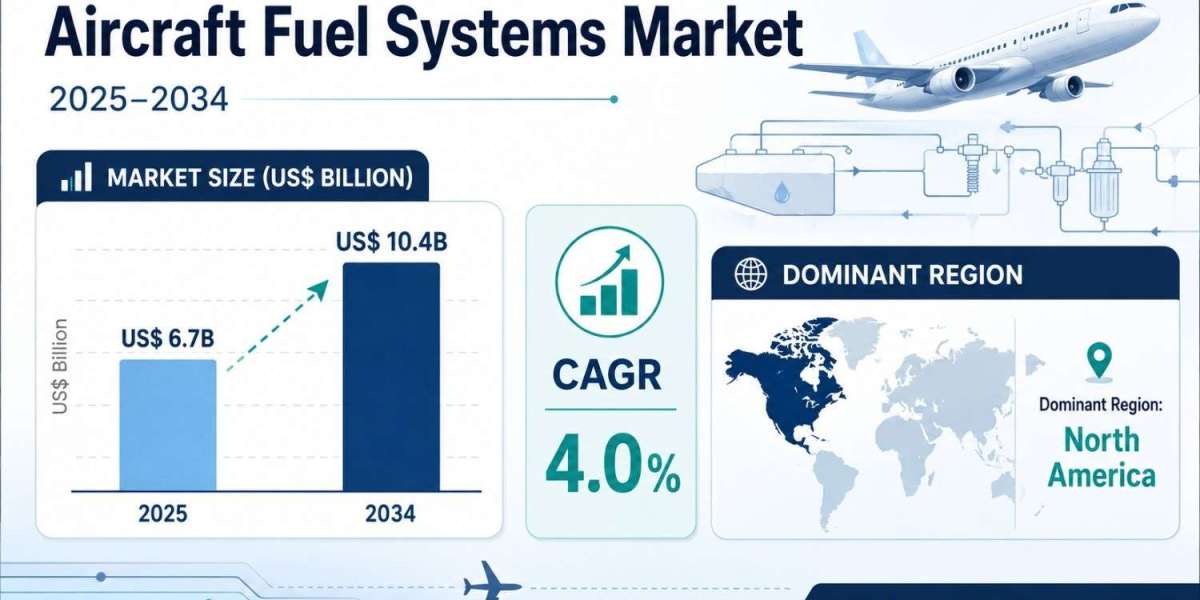

The Aircraft Fuel Systems Market is likely to grow from US$ 6.7 billion in 2025 to US$ 10.4 billion by 2034. The Aircraft Fuel Systems Market is expected to grow at a CAGR of 4.0% during 2026–2034. Market intelligence indicates steady demand from commercial aircraft, OE production, fuel efficiency, and safety systems.

Aircraft fuel systems are one of the most essential onboard systems because aircraft cannot sustain flight without reliable fuel storage, control, and delivery. The Aircraft Fuel Systems Market share landscape is shaped by suppliers competing on technological innovation, cost efficiency, measurement precision, safety, and weight optimization.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/aircraft-fuel-systems-market#form

Market Segmentation Analysis

The Aircraft Fuel Systems Market is segmented by Aircraft Type into Commercial Aircraft, Regional Aircraft, Military Aircraft, Helicopter, General Aviation, and UAV. Commercial aircraft are expected to remain dominant and fastest-growing throughout the study period, supported by fleet size and high production rates.

By Component Type, the market is segmented into Pipe, Pump, Inerting System, Valve, Gauging & Management System, Filters, Tank, Metering, and Other Components. Gauging & Management System is expected to retain the largest share through 2034, while Inerting System is likely to remain the fastest-growing component type.

By Technology Type, the market is segmented into Fuel Injection, Pump Feed, and Gravity Feed. Pump Feed is likely to remain the most attractive technology type during the study period. Its relevance is reinforced by adoption across modern commercial and military aircraft platforms.

By Engine Type, the market is segmented into Turbofan, Turboprop, and Other Engines. Turbofan is expected to retain the largest share in 2025 and the fastest growth by 2034. Demand is supported by commercial aircraft, military aircraft, regional aircraft, and business jets.

By Application Type, the market is segmented into Airframe and Engine. Airframe held the larger share because it covers fuel tanks, pumps, valves, vents, gauging systems, and transfer lines. Engine is expected to take the front seat in long-term growth due to fuel flow precision requirements.

By End-User Type, the market is segmented into OE and Aftermarket. OE is expected to remain dominant and faster-growing throughout the study period, driven by strong aircraft and aeroengine production, order backlogs, and advanced fuel systems for next-generation engines.

Regional Market Insights

North America is expected to remain the largest Aircraft Fuel Systems Market during the forecast period. Its lead is supported by major aircraft OEMs, Tier-1 players, aerospace manufacturing ecosystems, airlines, MRO providers, and engine manufacturers such as GE Aerospace and Pratt & Whitney.

Asia-Pacific is likely to grow at the fastest rate during 2026–2034. China and India are identified as regional growth contributors, while China’s focus on indigenous production is creating opportunity pools in the aircraft fuel systems market.

Emerging Trends Shaping the Aircraft Fuel Systems Market

Competition is increasingly influenced by fuel measurement precision, automation, safety architecture, and lightweight design. Modern fuel systems now feature digital quantity indication, automated fuel transfer and balancing, real-time diagnostics, and advanced control systems that support performance and reliability.

Recent product development is focused on efficiency, safety, environmental performance, SAF compatibility, and more-electric aircraft configurations. Manufacturers are also using lightweight composites and corrosion-resistant alloys to improve durability, reduce aircraft weight, and support fuel economy.

Key Growth Drivers of the Market

- Commercial aircraft demand is increasing fuel system requirements across the largest and fastest-growing aircraft segment.

- OE production and order backlogs are supporting demand for advanced systems used in new aircraft and aeroengines.

- Digital fuel monitoring is driving demand for Gauging & Management System components across modern aircraft.

- Safety requirements are increasing the relevance of inerting systems, leak detection, and fault-tolerant architectures.

- SAF compatibility and more-electric configurations are shaping supplier innovation and future product development.

Competitive Landscape

Top Companies in the Market

Eaton Corporation Plc

Parker Hannifin Corporation

RTX Corporation

Safran S.A.

Woodward, Inc.

Honeywell International Inc.

Crane Company

Triumph Group, Inc.

PTI Technologies (ESCO Technologies)

Robertson Fuel Systems, LLC (Heico)

Conclusion and Strategic Outlook

The Aircraft Fuel Systems Market is expected to reach US$ 10.4 billion by 2034, growing at a CAGR of 4.0% during 2026–2034. The competitive landscape is shaped by technology innovation, cost efficiency, safety standards, precision, and weight optimization. Strategic demand will remain tied to modern aircraft platforms and advanced fuel management systems.

FAQs – Aircraft Fuel Systems Market

What is the Aircraft Fuel Systems Market value by 2034?

The Aircraft Fuel Systems Market is likely to reach US$ 10.4 billion by 2034. It was valued at US$ 6.7 billion in 2025.

What is the CAGR of the Aircraft Fuel Systems Market?

The Aircraft Fuel Systems Market is expected to grow at a CAGR of 4.0% during 2026–2034. This reflects steady growth across aircraft platforms and end-user channels.

What are the major growth drivers?

Growth is driven by commercial aircraft production, fleet modernization, advanced fuel monitoring, safety requirements, and OE demand. SAF compatibility and more-electric aircraft configurations are also influencing product development.

Which region has the strongest market position?

North America is expected to remain the largest market during the forecast period. Its position is supported by OEMs, Tier-1 suppliers, MRO providers, airlines, and engine manufacturers.

What is the competitive and investment outlook?

The market is moderately concentrated, with leading players competing on innovation, cost efficiency, fuel measurement precision, safety, and weight optimization. Investment focus is likely to remain aligned with advanced, lightweight, and digitally enabled fuel systems.